")

KUALA LUMPUR, Sept 29 — The prices of houses in Malaysia will likely not drop significantly, due to continued demand from first-time buyers for affordable housing and as developers roll out more affordably-priced projects, Bank Negara Malaysia (BNM) said today.

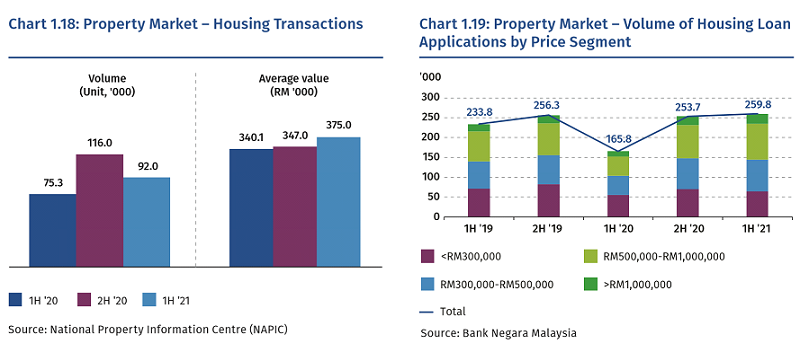

In its Financial Stability Review for the first half of 2021, BNM examined recent trends in the residential property market, observing that the number of transactions or houses bought had decreased this year.

Based on the National Property Information Centre’s (Napic) data, 75,300 houses were sold with an average transaction value of RM340,100 in the first half of 2020, which then increased to 116,000 housing transactions with an average transaction value of RM347,000 in the second half of 2020.

This then dropped to 92,000 housing transactions in the first half of 2021 or from January to June this year, but with a higher average transaction value of RM375,000.

As compared to the second half of 2020, BNM said the first half of 2021 saw slower housing transactions as the effect from positive response to the government’s home ownership incentives had subsided.

In explaining the lesser number of houses sold and bought from January to June this year, BNM highlighted that market activity from April to June was weighed down by tighter movement restrictions and operational frictions after Covid-19 cases surged.

BNM however said the number of housing transactions during these months had received a boost by the anticipation then that the Home Ownership Campaign would expire by the end of May 2021. (The Home Ownership Campaign has since then been extended to December 31, 2021.)

Even as the housing market activity slowed down, the average transaction values had grown at a stronger pace, as transactions for housing priced below RM500,000 accounted for more than 80 per cent of housing transactions.

In line with the slower market activity, the number of unsold houses had rose from 167,104 units in the fourth quarter of 2020, to 181,460 units in the second quarter of 2021, largely due to houses priced above RM300,000 and under-construction serviced apartments, and partly also due to new housing projects launched in previous quarters that experienced slower sales during this period, BNM said.

But it noted that the housing market’s observers expect activity to pick up with the gradual easing of movement restrictions and recovery in economic activities, as seen previously in the second half of 2020.

With developers expected to offer new housing with more affordable prices and continued demand from those purchasing their first home, BNM said there would be reduced risks of significant drop in housing prices.

“Incoming supply of newly-launched residential properties would likely shift towards the mass market price segments, as seen in the higher share of properties priced at RM500,000 and below,” it said, noting that the average percentage of such houses for 2015 to 2019 is 65.9 per cent and that it was 71.6 per cent in the first half of 2021.

“Such adjustments will continue to reduce demand-supply mismatches and improve overall housing affordability.

“Along with sustained demand among first-time house buyers, this is expected to mitigate risks of a significant house price correction,” BNM said, referring to Napic’s latest release using preliminary estimates that said house price growth is likely to have remained flat in the first half of 2021. BNM added that the housing market is expected to recover heading into 2022.

Among other things, BNM had also noted that demand for housing loans has now recovered to above pre-Covid-19 pandemic levels, as the number of applications for housing loans had in the first half of 2021 increased across most price categories of residential properties, as compared to the second half of 2020.

“Approval rates have also broadly recovered closer to levels recorded before the pandemic (overall approval rate in 1H 2021: 73.2 per cent; 2020: 71.5 per cent; 2013-2019 average: 75.5 per cent), except for properties priced above RM1 million where approval rates have continued to reflect the more cautious risk appetite of banks.”

What are the risks if housing prices fall significantly?

A significant house price correction would carry risks of undermining household balance sheets and increase potential losses to banks, but such risks remain manageable, BNM said.

The risks to banks are further controlled as they have limited exposure to “household investors”—those who have more than one housing loan or who buy houses to invest—who took up property loans.

This is because household investors may choose to not pay the housing loan from banks, if there is a “negative equity” scenario where the value of the house they invested in falls lower than the amount they still owe the banks.

“In particular, risks from household investors in the housing market remained contained amid prevailing low interest rates. Such borrowers have higher incentives to default if house prices were to decline and fall into negative equity or they face a loss of rental income,” BNM said.

While the percentage of property loans given to household investors had risen slightly from pre-pandemic levels of 13.3 per cent in December 2019 to 13.6 per cent in December 2020 and currently to 13.7 per cent of overall banking system loans, BNM said the exposure of banks in housing loans to owner-occupiers has continued to grow faster than that of exposure to household investors.

The annual growth rate for banks’ housing loan exposures to owner-occupiers is now 8.4 per cent (as compared to 8.7 per cent in December 2020) and to household investors is now at 5.2 per cent (5.0 per cent in December 2020).

“So far, household investors are predominantly higher-income earners who are typically more resilient to income shocks.

The average loan-to-value (LTV) ratio of outstanding housing loans by household investors also remained relatively low and stable (54.8 per cent; December 2020: 54.9 per cent), thus preserving ample buffers against a potential decline in house prices

“Some pockets of household investors may be experiencing challenges in servicing their debt based on repayment assistance data, but risks to banks stemming from these borrowers are judged to be low, given the small share of investors in negative equity at less than one per cent of total housing loans.

“Despite low interest rates, existing macroprudential measures are believed to have reinforced prudent lending behaviour among banks and mitigated a credit-fuelled increase in residential property prices such as that experienced in some other jurisdictions,” it said.