KUALA LUMPUR, Feb 6 — Maybank’s HouzKEY scheme offers Malaysians a way to own a home without paying down payment; they just pay monthly rental that is slightly higher than a housing loan instalment.

How does that work?

Here are the details as shared by Maybank managing director of real estate ventures Sally Lye Saw Im in a recent interview with Malay Mail:

HouzKEY is based on an Islamic leasing concept where participants will be able to rent from Maybank until they decide to buy the house.

HouzKEY’s transparent nature is shown with Maybank buying properties from developers at the exact same price that Malaysians would get if they went directly to the developers. And this price will be used to calculate the monthly rental rate.

HouzKEY applicants can choose the unit they wish to stay in and request a visit to view it, with Maybank saying it can respond within 24 hours on whether the application is approved. For popular properties that others are also applying for, applicants will be put on a waiting list and the first person to sign the lease agreement will get it.

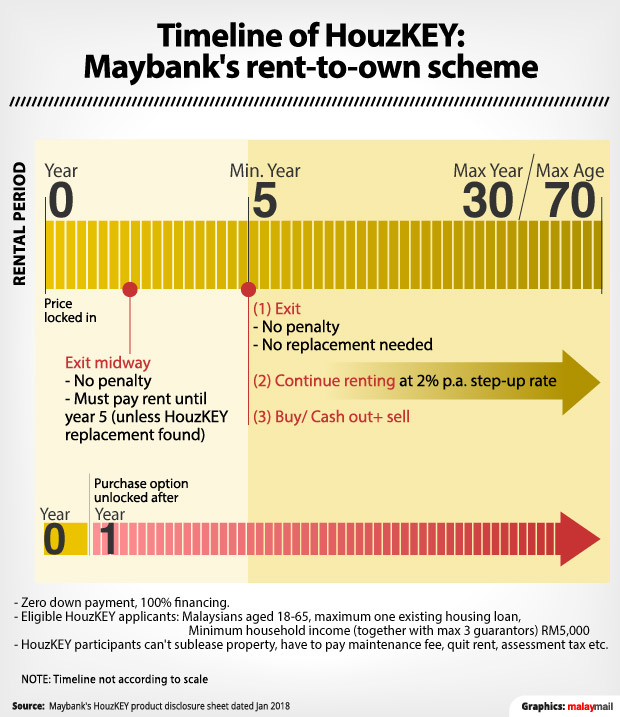

When signing a leasing contract with Maybank for the property they intend to eventually own, HouzKEY applicants can choose a rental period ranging from a minimum five years to a maximum 30 years at their own choice. If age permits (the maximum period is capped at 70 years old), the savvy customer should choose the longest leasing period possible, as the monthly rentals spread out over more years would be cheaper.

The calculations for HouzKEY’s monthly rental rates and for a typical housing loan’s monthly instalments are the same, and is based on the same mortgage calculator at the same rates, Lye revealed.

But why is the monthly rental higher than housing loan instalments?

That is because a housing loan usually only allows buyers to borrow up to 90 per cent of a property purchase price and requires them to pay the remaining 10 per cent on their own, while HouzKEY gives 100 per cent financing which would free buyers from having to pay for a down payment, Lye explains.

In other words, what would usually be the down payment is already included in the total 100 per cent sum in HouzKEY and will be repaid through the monthly rentals.

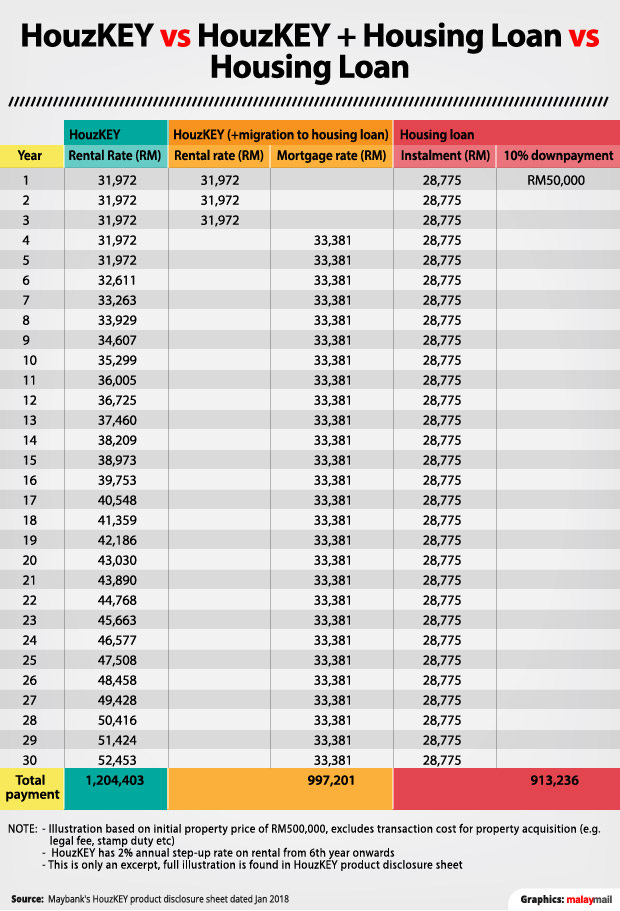

In Maybank’s illustration for a RM500,000 house, a borrower who took a 30-year housing loan will have to pay the RM50,000 down payment on their own and RM28,775 in monthly instalments for the first year, and RM28,775 in instalments every year after that.

In contrast, a HouzKEY participant who rents for 30 years will pay RM31,972 annually for the first five years, and at annual rental rates that climb up incrementally at two per cent per annum from the sixth year onwards (for example, RM32,611 in sixth year and RM33,263 in seventh year) until it hits RM52,453 in the 30th year. But if the HouzKEY participant switches to a housing loan with Maybank from the fourth year onwards, they will pay a fixed annual rental rate of RM33,381 until the end of the 30th year.

By the end of the 30-year period, the person who took a housing loan would have paid a total of RM913,236, while the HouzKEY participant who rented from Maybank for 30 years would have paid a total of RM1,204,403 in rental. The HouzKEY participant who switched to a mortgage midway would have paid RM997,201 in rental and instalment.

“We are trying to help the customers — those that are currently renting a house but they want to own a house, but they cannot own a house because they don’t have the initial down payment. What we are trying to say is, now Maybank gives you an opportunity to own a house with very, very minimal initial payment,” Lye said.

A unique proposition

A unique proposition

House buyers usually take housing loans and stomach the down payment, in order to lock in the property price that would otherwise continue to rise as the property grows in value.

But HouzKEY uniquely also gives participants the option to purchase the house later at a price that is already fixed when they sign the leasing contract.

“In HouzKEY, you lock in the price too, same thing, and more importantly every month when you pay rental in HouzKEY, this rental will pay down the purchase price from the original price,” Lye said.

She said every month of rent — even from the first month itself — will help trim down the actual purchase price when HouzKEY participants do decide to buy, much like how monthly instalments cut down the total sum of a housing loan owed by the borrower to the bank.

Okay, so what do you have to pay?

Compared to taking a housing loan and needing to self-fund up to 15 per cent of the property price (down payment and other fees), HouzKEY participants only need to pay Maybank an upfront refundable three-month rental deposit, which is roughly around 2 per cent of the property price. As for legal fees and stamp duty for the lease, these can be part of the monthly rentals.

Just like a homeowner, a HouzKEY participant will, while renting, have to pay for things such as utilities, maintenance fee, quit rent and assessment tax on the property.

“From day one, we don’t treat you as tenant, we treat you as owner already, even though legally we are the owner,” Lye said, pointing out that the HouzKEY participant enjoys the rights akin to a house owner, such as the right to renovate and the right to enjoy the future capital gains to be made when the property is sold.

Unlike normal renting arrangements where the tenant will not be allowed to renovate the landlord’s property, HouzKEY participants are allowed to carry out renovations after informing Maybank, even if they are still paying rental and have yet to switch to a mortgage.

Three choices after five years

Under the HouzKEY scheme, participants have to commit to renting for a minimum of five years, but, after renting it for at least one year, they can buy the property at the price that was pre-agreed at the time the leasing agreement was signed.

Option 1: Continue renting with incremental hikes

After sticking through with the scheme for five years, participants will have three options, including to rent until the maximum tenure of 30 years and to buy the property at a nominal sum of RM1 from Maybank at the end of the tenure.

But in hopes of encouraging homeownership, Maybank will impose a two per cent per annum increase on rental from the sixth year onwards if HouzKEY participants decide to just continue renting instead of buying.

As an example, a RM2,000 monthly rental will in the sixth year be RM2,040, which will then rise to RM2,080.80 per month in the seventh year and RM2,122.40 and RM2,164.90 in the eighth year and ninth year, and so on. This means the HouzKEY participant will have to pay a top-up in the security deposit, on top of the refundable three-month rental deposit previously paid.

“If you continue renting until 30 years, there will be the step-up. If you decide to move to mortgage, there is no step-up,” Lye said, pointing out that switching to a mortgage would be cheaper than continuing to rent with the increased rates.

Option 2: Walk away

You can walk away at any time from the fifth year onwards, with no penalties imposed and with the three months’ rental deposit refunded. You will not be required to find a replacement HouzKEY participant.

Option 3: Buy / Cash out (Buy and sell off)

You can buy the property either through cash or by switching to a housing loan with Maybank — again without having to pay a down payment. Or you can cash-out and enjoy the profit after selling the property that by then would have appreciated in value. This option can be exercised even earlier, after at least a year of renting.

Lye said the switch to a mortgage with Maybank will be a seamless and expedited process, noting: “So under this migration to Maybank mortgage, you are not required to come out with a 10 per cent (down payment) anymore. You don’t need to go through a credit assessment and all that. So technically you are just moving from one product to another, you are refinancing.

“So assuming after five years, whatever rental that you have paid contributes to the principal of the amount, then the amount when you move to mortgage will be lower and your instalment will be lower as well. So this HouzKEY is for you to prepare yourself financially with your good payment track record,” she said.

In a normal rental arrangement, the landlord will benefit from the property’s appreciation in value over the years as he or she is the owner, while the tenant who chooses to buy the property over from the landlord will have to pay a price that is higher than what the landlord originally paid long ago.

Under the cash-out option, HouzKEY participants can buy the property from Maybank on paper and then sell it off to another buyer, pocketing the gain based on the difference between the higher current market price and the lower purchase price pre-fixed years ago under HouzKEY. They can also appoint Maybank to find a buyer for their property, and benefit from the same appreciation in value that is typically enjoyed only by those are homeowners by way of housing loans.

If you change your mind...

If you change your mind...

One key benefit of HouzKEY is the flexibility it affords its participants, where it has a relatively shorter lock-in period of only five years, as compared to a housing loan where borrowers will be tied down in debt for up to 35 years until they clear it off.

For those who decide to exit HouzKEY before the first five years is up, there will be no penalty but they will have to pay rental for the remaining tenure.

Even though Maybank is not obliged to do so, it will try to find a replacement tenant under the HouzKEY scheme, Lye said. If a replacement tenant is found, Maybank will waive the remaining rental sum that the person exiting initially had to clear off.

“So we also give the individual an option, some people say investing in property, buying a property is a lifetime commitment — yes; but with HouzKEY, you can change your mind after five years. No facility in Malaysia will allow you to change your mind. So that’s another key difference between mortgage and HouzKEY,” she said.

Zero stamp duty for purchase, early RPGT start-date

Lye said Maybank had lobbied hard to the Finance Ministry to secure additional benefits for HouzKEY participants, convincing the government to grant stamp duty exemption when the bank transfers properties to customers who buy under HouzKEY. (For example, stamp duty for transfer of a property sold at RM500,000 would have cost RM9,000).

Maybank also managed to get the ministry to agree to calculate the acquisition date for HouzKEY participants from the day they sign the lease agreement with the bank, instead of from the latter date when they actually decide to buy under HouzKEY. (Usually, the date of acquisition is calculated from the day the buyer signs an agreement to buy from a developer).

This means that the HouzKEY participants could potentially pay less Real Property Gains Tax (RPGT) when they resell the property, as the tax on profits from property sales is dependent on how quickly the property is sold.

The current RPGT rate on profits made by a Malaysian is 30 per cent if the property is sold off within three years of purchase, 20 per cent in the fourth year, 15 per cent in the fifth year, and zero from the sixth year onwards.