growthin Kuala Lumpur February 12, 2020. u00e2u20acu2022 Bernama pic")

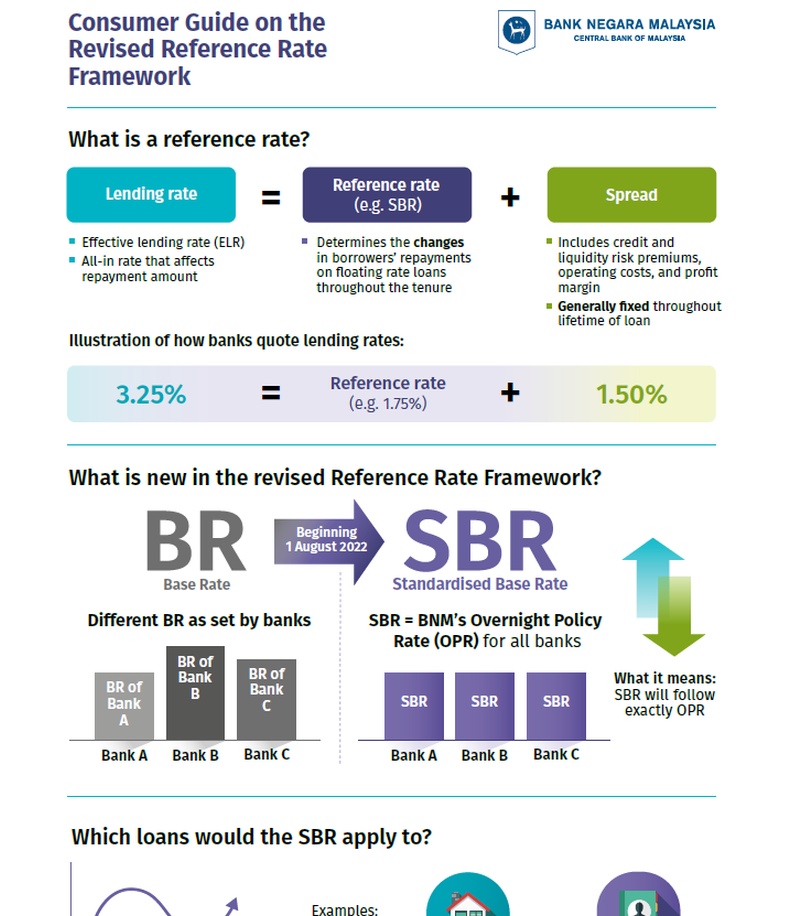

KUALA LUMPUR, Aug 11 ― Bank Negara Malaysia (BNM) has released the revised Reference Rate Framework, under which the Standardised Base Rate will replace the Base Rate (BR) as the reference rate for new retail floating-rate loans from August 1, 2022.

The central bank said under the revised Reference Rate Framework, the Standardised Base Rate will be used as the common reference rate for all financial institutions for their new retail floating-rate loans and will be linked solely to the overnight policy rate (OPR).

Changes to the Standardised Base Rate will therefore only occur following changes in the OPR, which is determined by BNM’s monetary policy committee, it added.

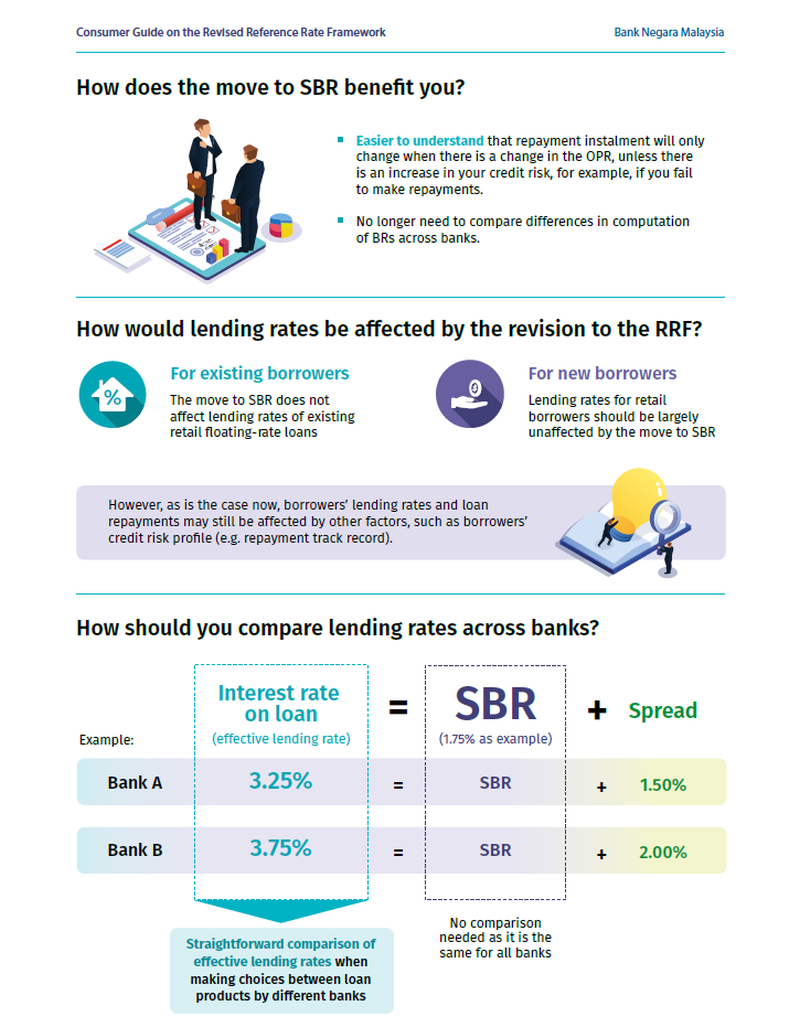

Governor Datuk Nor Shamsiah Mohd Yunus said consumers would find it easier to understand changes in their loan repayments as the OPR will be the only driver of the Standardised Base Rate.

“The Standardised Base Rate will also facilitate effective monetary policy transmission as complete adjustments to retail loan repayments will take effect following a change in the OPR,” she said in a statement.

The Standardised Base Rate will take effect as the reference rate for the pricing of new retail floating-rate loans and the refinancing of existing loans from August 1, 2022, to provide sufficient time for financial institutions to undertake the necessary preparations and system enhancements to ensure a smooth implementation of the revised framework.

BNM said the shift towards the Standardised Base Rate following the revision in the Reference Rate Framework does not represent a change in the monetary policy stance of BNM’s monetary policy committee.

BNM said the shift towards the Standardised Base Rate following the revision in the Reference Rate Framework does not represent a change in the monetary policy stance of BNM’s monetary policy committee.

Other components of loan pricing such as borrower’s credit risk, liquidity risk premium, operating costs, profit margin, and other costs will continue to be reflected in the spread above the Standardised Base Rate, said the central bank.

BNM said the shift towards the Standardised Base Rate will have no impact on the effective lending rates of existing retail loans, which will continue to be referenced against the Base Rate (BR) and Base Lending Rate (BLR).

After the effective date, the BR and BLR will move exactly in tandem with the Standardised Base Rate as any adjustments to the Standardised Base Rate will simultaneously be reflected in the corresponding adjustments to the BR and BLR.

“As such, financial institutions will continue to display their BR and BLR, in addition to the Standardised Base Rate, at all branches and websites after the effective date for customers’ reference,” said BNM.

The central bank said “new retail borrowers should be largely unaffected by this revision, as effective lending rates for new borrowers would continue to be competitively determined and influenced by multiple factors, including a financial institution’s assessment of a borrower’s credit standing, funding conditions and business strategies.” ― Bernama