")

")

KUALA LUMPUR, July 14 — Malaysians can finally start applying for the six-month loan relief programme from banks which allows them to start making full payments again only in 2022.

But what do you need to know before deciding whether to take up the option?

If you are struggling with finances right now or expect to have difficulties paying your bank loans over the coming months this year, this six-month loan relief announced last month (June 28) under the Pemulih economic package may provide some temporary and near-instant financial relief.

But is this plan suitable for everyone?

Malay Mail combed through the FAQs and information about Covid-19 payment assistance including the plans provided by three of Malaysia’s largest banks (Maybank, CIMB, Public Bank) on their websites as well as general information from Bank Negara Malaysia, and here’s a quick summary of the main points you should know:

1. How does the Pemulih loan payment assistance work?

Generally, you are given two options: a) A six-month moratorium on your loan, which means you will not be making any payments for six months but will defer or postpone making payments until after the six-month period ends; or b) A 50 per cent reduction in monthly loan installments for six months.

Note: This applies to bank loans in general, but different banks may offer different payment assistance for different types of financing such as car loans or credit card bills. (Check your own banks’ FAQ and terms and conditions.)

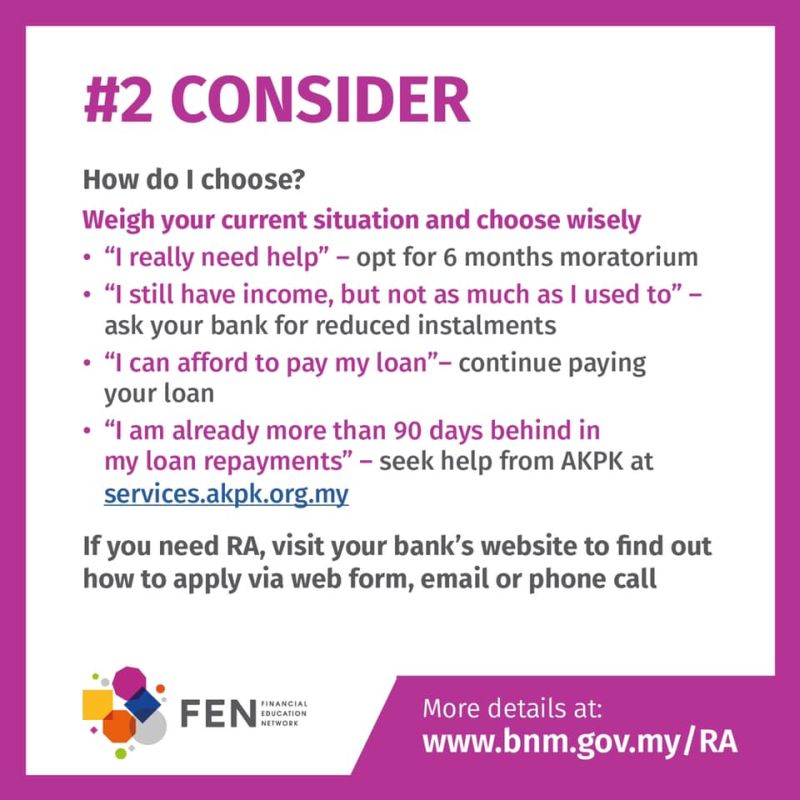

2. Who can ask for the six-month moratorium or six-month half payment?

Individuals, small medium enterprises (SMEs), and microenterprises can apply from July 7 to their respective banks to “opt-in” for the six-month moratorium or halved monthly installments.

This is open to all individuals from all income brackets — B40 low-income category, M40 mid-income category or T20 high-income category.

Your application for the six-month moratorium or the 50 per cent monthly loan instalments under Pemulih will be automatically approved, without you needing to provide any supporting documents. The banks will essentially be relying on borrowers’ self-declarations.

(Previously, Malaysia’s banks had from April to September 30, 2020 given a six-month blanket automatic moratorium to all eligible borrowers, with the banks then shifting subsequently to a targeted repayment assistance to help borrowers who had reduced income or had lost their jobs.

In comparison, under the loan moratorium option in the Pemulih package that kicked in from July 2021, the prime minister said it does not come with the condition of reduced income and there will also be no need to check whether a borrower has lost his/her job.

It is still best to be honest, as for example, CIMB’s terms and conditions on the moratorium or reduced installment options for housing loans and personal loans state that CIMB may change or modify payment terms or cancel a borrower’s participation if found that the borrower had given “false, misleading or incomplete information” in the application for the option. Maybank, in its terms and conditions to borrowers, similarly states that it reserves the right to modify or cancel the repayment assistance if the application for such aid contained “false, misleading or incomplete representation.”)

Depending on your bank and whether you applied through online or other methods, notification of successful approval can be as quick as within 24 hours (for online applications for Public Bank borrowers) or within five days for individuals and within 14 days for companies (for non-online applications for Public Bank borrowers). Maybank said borrowers would be informed within five days of the status of their applications.

Bank Negara Malaysia also states that banks will process the opt-in applications within five calendar days for individual borrowers and within 14 calendar days for microenterprises and SMES, adding that borrowers who have not received any response from their banks within these timeframe can file a complaint to Bank Negara Malaysia via the website bnm.my/RAsurvey by filling up the form there.

3. Who is not eligible for the six-month moratorium or six-month half payment?

However, do note that this repayment assistance is not open to borrowers who have been overdue in their payments for more than 90 days (which would mean owing payments for more than three months), or those undergoing bankruptcy or winding-up proceedings.

Banks may have additional details. For example, Maybank’s FAQ document also states that eligible borrowers are those whose loans were approved on or before June 30, 2021, and that they must not be already declared bankrupt or under bankruptcy proceedings.

Public Bank’s FAQ states that eligible borrowers are those whose loans were approved on or before July 1, 2021, and that only individuals who are not bankrupt and companies that are not wound up can request to opt-in for the six-month moratorium or reduced 50 per cent installment.

Similar information can be found in CIMB’s terms and conditions documents for housing loans and personal loans, where eligible customers are those who have not been owing loan repayments for more than 90 days, and who are not currently under rehabilitation with the Credit Counselling and Debt Management Agency (AKPK) — an agency set up by Bank Negara Malaysia.

(Don’t be alarmed if you are not eligible for the moratorium, as Maybank’s FAQ for example states that you can contact the bank to work out a repayment assistance plan that would be more suitable for you, and that you can also seek help from AKPK that provides free financial advice and assistance to help manage finances. Public Bank similarly said such borrowers can contact AKPK, which provides free services such as for debt restructuring.

Maybank also said borrowers who are facing difficulties in paying the amount previously agreed with AKPK can approach the agency.)

4. This is the most important thing

Ok, if you are eligible to apply for the six-month loan moratorium or six-month halved monthly installments, you should bear in mind that interest (or simple interest) will continue to be charged and accumulate, and your loan tenure or repayment period may get extended.

Bank Negara Malaysia has already said that banks will not charge compounding interest (interest on interest) or any penalty interest during the six months.

Compound interest is when interest is charged on the loan’s principal amount and the interest that would have been due, while simple interest is interest charged on the loan’s principal amount.

Here’s an example of how the loan you took will become more costly as a whole, based on an illustration by Maybank of how a six-month moratorium or six-month halved instalments would affect a hypothetical borrower who took a 35-year loan for RM150,000, and has 30 years left of payments to make at a variable interest rate of 3.25 per cent (assuming it does not change).

In this example, the hypothetical borrower has a remaining balance of RM137,499 to repay over the next 30 years.

Instead of paying interest of RM77,927 over 30 years with full monthly installment payments of RM598 in this example, a borrower will have eventually paid RM83,931 in interest (or about RM6,000 more) if zero payment was made for six months using the moratorium option and if payments of RM598 were resumed from the seventh month onwards, with the loan to be fully-cleared 31.3 years later instead of 30 years.

If the borrower only paid half of monthly instalments for six months before resuming full RM598 instalment payments, the additional interest of about RM2,970 accumulated will result in an eventual interest cost of RM80,897 paid over 30.7 years.

Maybank also gave examples of scenarios of fixed-rate personal loans where a six-month loan moratorium would result in the loan tenure ending six months later but without increases in the number of loan instalments or overall interest paid, while a six-month halved instalment plan would result in the loan tenure extended for three more months of full instalments to be paid but also without increase in overall interest paid.

In Maybank’s example of a hypothetical RM50,000 nine-year hire purchase loan or vehicle loan at a fixed interest rate of 2.8 per cent with three years (36 months) left to pay a RM19,441 sum, a six-month halved payment option will result in an additional RM258 being paid with the loan tenure extended to 39 months, while a six-month moratorium will result in an additional RM471 being paid with the loan tenure extended to 42 months.

These are just examples for illustration purposes, as the actual length of loan tenure extension and interest charges will be different, depending on the interest rate of the loan and the remaining tenure.

Earlier in the FAQ, Maybank advised customers to continue with their current repayments if they can afford to do so instead of opting-in at this point in time as the six-month plan would increase overall borrowing costs, pointing out that borrowers can still opt for repayment assistance plans in the future if they later face financial difficulties.

Public Bank also provided an example of a loan with RM100,000 left to be paid over 120 months with interest rate of 3.07 per cent and monthly installments of RM1,000, noting that a six-month moratorium would result in an estimated additional cost of RM2,087 with the tenure to end six months later, and a six-month halved payment would result in additional cost of RM1,031 with the tenure to end three months later.

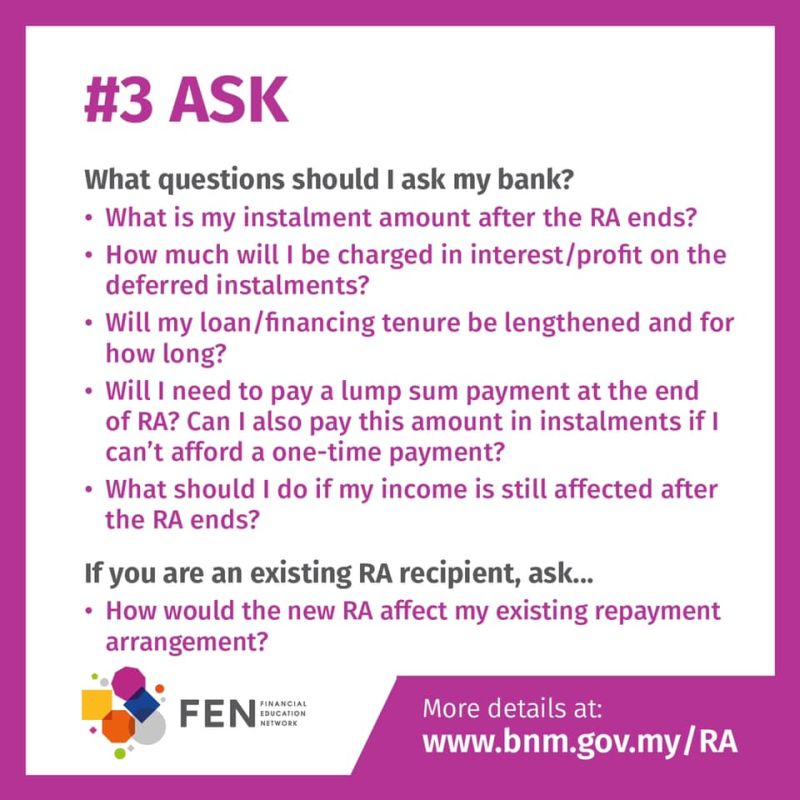

In seeking to help borrowers make an informed decision, CIMB said that both the six-month moratorium and six-month halved payment options for a property loan or personal loan would not result in the loan tenure being extended, saying that borrowers may instead have to pay a lump sum or higher amount at the end of the loan’s tenure to settle the entire loan.

Whichever option is taken up for the six-month period, borrowers will be able to gain a short-term relief, but will be paying more money back to the banks in the form of interest for the loan.

In the same FAQ, CIMB said borrowers who find themselves unable to pay the final amount at the end of the loan should contact the bank as soon as possible to discuss payment options.

5. So should you ask for the loan moratorium or halved payments for six months? What about credit ratings?

Just like Bank Negara Malaysia, the individual banks (such as Maybank, CIMB and Public Bank) have assured borrowers that their credit ratings or Central Credit Reference Information System (CCRIS) record or status would not be affected by the decision to opt-in for the moratorium or repayment assistance plan.

Maybank for example states that the moratorium or repayment assistance plan would not affect the CCRIS record if the borrower is not overdue for more than 90 days, while Public Bank states that opting-in would not result in a borrower’s account as being tagged or reported as rescheduled and restructured in CCRIS.

If you are facing financial difficulties and need the temporary relief until your financial situation improves, you can opt in, after having read and understood all the necessary information such as the FAQ and terms and conditions. If you are unsure and need guidance or want to explore alternatives, you can consult AKPK which gives free advice.

Just as the banks have been careful to stress the need to make an informed decision, Bank Negara Malaysia has also pointed out that borrowers who can afford to continue their loan repayments should do so, as this would be in their best interest as resuming repayments would reduce the overall cost of borrowings.

Maybank, for example, states that borrowers can opt out at any time after joining the loan moratorium or halved payment plan, by simply resuming full payments and without the need to notify the bank.

CIMB also encourages borrowers to contact the bank as soon as their financial situation improves and reminded that revising the monthly payment will help reduce the overall cost of the loan, while Public Bank also said borrowers may write or email the bank to cancel the repayment assistance.

6. How soon can the six-month period start? And what happens when it ends?

The six-month moratorium or six-month halved installments can start as early as July, if you need the relief from this month itself.

For example, CIMB states that borrowers who applied in July for the six-month relief can let the bank know if they wish to have the relief start in July itself. The bank says the six-month period starts from the month immediately after the bank confirms the borrower’s participation in the six-month moratorium or halved monthly installments.

Public Bank’s FAQ states that borrowers who applied to opt-in can contact the bank for reimbursement of the July loan installment if they had paid it when it was due in July and if they need the reimbursement.

For both the six-month moratorium and the 50 per cent reduction in monthly installments, Public Bank’s illustration shows that the six-month duration will depend on the month that borrowers made the request to opt-in (during the July 2021 to December 2021 period).

For example, a borrower who requested in July 2021 to opt-in, the six-month period will run from August 2021 to January 2022 and borrowers will have to resume normal and full payments in February 2022 and onwards. A borrower who requested in December 2021 to opt in will see the moratorium or halved installments run from January to June 2022, and have to resume full payments in July 2022 onwards.

In general, Maybank states that opt-in requests received on or before the 20th of months from August 2021 onwards will take effect in the same month, while the six-month period will only kick in the next month if opt-in requests are received after the 20th of a month and borrowers should continue paying before the six-month period starts. Maybank confirmed it can make reimbursements for July installments paid before the moratorium opt-in option was available from July 7.

When the six-month period for the options of moratorium or halved payment ends for a borrower, Maybank said the borrower would then have to pay the same or revised lower monthly installment but with the loan tenure extended to ensure the monthly payments stay manageable.

However, borrowers can also contact Maybank if they wish to maintain the original loan tenure after the six-month period ends, but this would also result in the monthly instalments being revised to be higher.

7. Other loan repayment assistance options, eg credit cards

For credit card bills, the banks seem to provide the option of converting your credit card’s outstanding balance into a term loan which would be paid in installments over many months, if you are having trouble clearing your credit card bills now.

Credit card users would then have the option of applying for the six-month moratorium or six-month halved payments if they need to, after the credit card balance is converted into a term loan.

CIMB, for example, allows credit card borrowers to choose between repaying their outstanding balance over a 12-month, 24-month or maximum 36-month period with interest rate of 13 per cent per annum but with this option being available up to August 31.

While CIMB customers can continue to use their credit cards, the outstanding balance (which was converted into term loan) is still part of the credit limit, and the monthly installments of the term loan will be part of the minimum monthly payment for the credit card that customers must pay.

For credit card users who apply for help to repay, CIMB gave an example that showed customers would as a whole be paying an increased sum in interest if they opted for the six-month moratorium or halved payments on the installments for the term loan which was converted from the outstanding balance.

Similarly, Public Bank also allows credit card users to apply to make a one-time conversion of their outstanding balance to a term loan of up to 36 months at a 13 per cent per annum, and allow them to further apply for the six-month moratorium or halved payment options if they still have difficulties paying the term loan installments for the converted credit card balance.

The same eligibility criteria such as not being a bankrupt applies, and the CCRIS record would again not be affected.

For Maybank, credit card users who need assistance can have their outstanding balance converted to be repaid over a 36-month period through instalments, with the outstanding balance required to be at least RM500 to be converted.

Just as for repayment assistance for other types of loans, Maybank credit card users have to not be currently under rehabilitation with AKPK for their credit card bills or be an undischarged bankrupt or subject to any bankruptcy proceedings.

For Maybank users who had already missed paying their credit card installments for more than 90 days at the date of their application for repayment assistance, their application requires them to agree for Maybank to offer them a customised solution that is more suited to their financial circumstances, including possibly sharing their credit card details to AKPK for further debt management advice and allowing AKPK to access their CCRIS information.

In other words, those who seek help would still receive help tailored according to their financial situation.

The key message that seems to stand out is to speak to your respective banks to see what alternative arrangements can be made to help you avoid being credit impaired when you face financial difficulties at any point of time, with Public Bank for example offering further flexibility under its separate Targeted Repayment Assistance that will be available until December 31, 2021 to eligible individual and business borrowers.

Under this alternative scheme by Public Bank, their borrowers can opt for a six-month arrangement of only paying 25 per cent, or 50 per cent or 75 per cent of their usual loan instalments, and even have the fourth option of making their own proposals for any rescheduling and restructuring arrangements to the banks.

Conclusion

If you are not sure where to start, visit Bank Negara Malaysia’s website where it lists the links to individual banks’ websites for details on repayment assistance plans. Or contact AKPK for free advice.