")

KUALA LUMPUR, July 1 — It’s no secret that all of us would love for our savings to earn more money over time. Fixed deposits aren’t as liquid as savings accounts in the event you need immediate cash, but savings accounts basically give no interest these days…right?

As it turns out, there are several savings accounts in Malaysia that offer high interest rates — some with up to 6 per cent p.a.! Of course, there are certain conditions that need to be met to “unlock” the high interest, but there are also some savings accounts that easily offer more than 10 times the interest of a basic savings account.

Here are some of the best high interest savings accounts in Malaysia.

Standard Chartered Privilege$aver

Interest rate: Tiered, up to 6 per cent p.a.

Interest rate: Tiered, up to 6 per cent p.a.

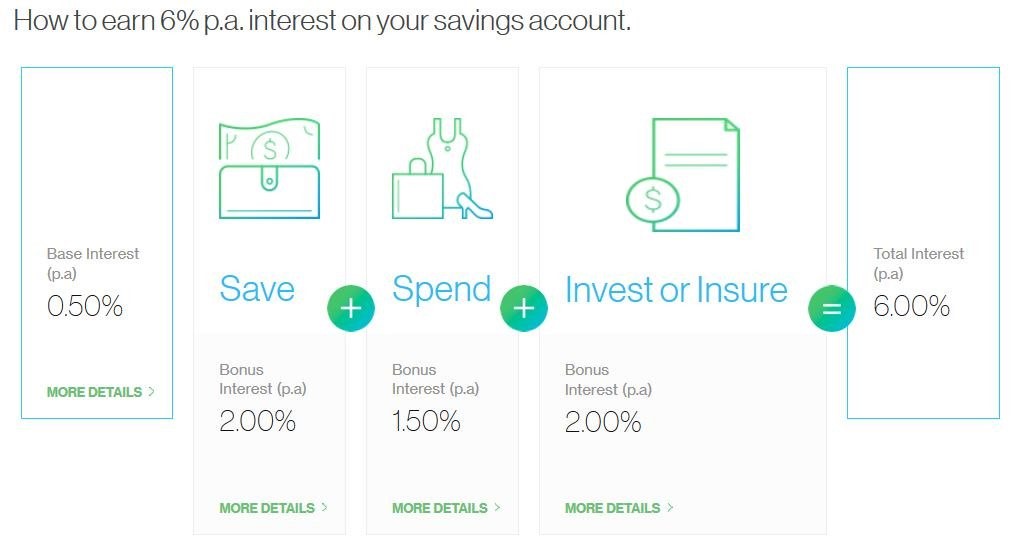

The Standard Chartered Privilege$aver savings account offers the highest interest rate on a savings account, if the account holder fulfils the conditions. There are three conditions required to increase the interest from the base 0.50 per cent p.a..

First, account holders need to deposit at least RM3,000 in fresh funds every month to unlock an additional 2 per cent p.a. interest. A further 1.50 per cent p.a. interest will be credited when you spend at least RM1,000 with your Standard Chartered credit card. Finally, unlock another 2 per cent p.a. when you purchase any regular monthly investment or insurance policy from StanChart with a minimum payment of RM1,000.

At 6 per cent p.a., you’ll be earning a huge chunk of interest each month. A good way to hit a minimum of 2.5 per centp.a. interest is to use this account as your salary deposit account — you just need to inform your HR department for this. It’s not a stretch to spend with StanChart’s credit cards — its JustOne Platinum and Liverpool FC Cashback credit cards also yield cashback as you spend, so you could be stacking quite a bit of money every month!

Do note, though, that the Privilege$aver campaign will end on 31 December 2019. It was extended from 2018, so there may be a chance that StanChart extends this again.

Interest rate: Tiered, up to 4.1 per cent p.a.

Interest rate: Tiered, up to 4.1 per cent p.a.

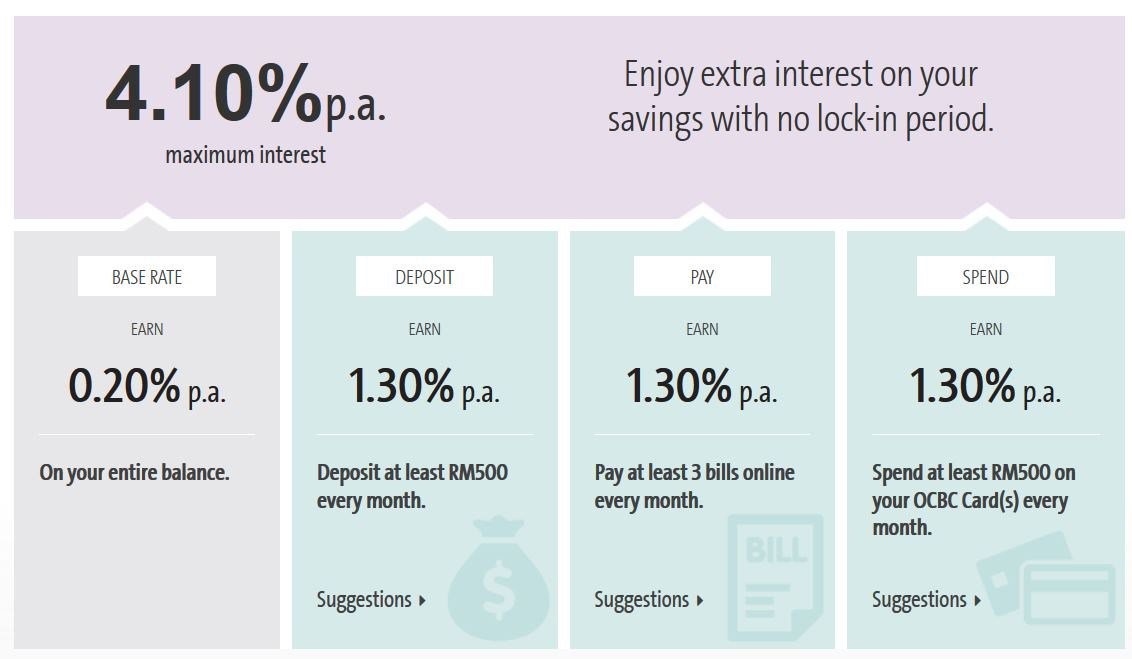

Like the StanChart Privilege Saver, OCBC offers bonus interest when you perform certain transactions with your OCBC online banking account as well as OCBC credit or debit cards. The base interest is low at 0.2 per cent p.a., but the three actions all yield a bonus interest of 1.3 per cent p.a. each. Fulfil all three actions in a month and enjoy a total of 4.1 per cent p.a. interest!

First, account holders simply need to deposit a minimum of RM500 every month into the OCBC 360 account to earn a 1.3 per cent p.a. bonus interest. An additional 1.3 per cent p.a. will be given when the account holder pays at least three bills with their OCBC online banking facility in a month. This includes credit card bills, loans, as well as JomPay bill payments! Finally, a further 1.3 per cent p.a. interest will be credited when you spend at least RM500 on your OCBC credit or debit card, brining the total interest to 4.1 per cent p.a. for that month.

Looking at the conditions, the OCBC 365 actually makes it easy to hit the 4.1 per cent p.a. interest. Enabling JomPay bill payments makes it easy to hit the three transactions required, while you can earn additional cashback for that RM500 spend for credit/debit cards with the OCBC 365 credit card, which offers 1 per cent cashback for the first RM1,000 charged.

Just note that multiple bill payments to the same biller in a single month will count as one transaction.

OCBC also has a Syariah-compliant variant with the same benefits, known as the OCBC Al-Amin 360, with a similar profit rate.

Interest rate: tiered, up to 3.5 per cent p.a.

If you’re looking to “park” a large sum of cash and earn the most interest with the least hassle, the Alliance SavePlus Account is the top choice. The only requirement to unlock a massive 3.5 per cent p.a. interest is to maintain account balances above RM100,000.

Even though it is technically classified as a current account, there really isn’t that much difference between the Alliance SavePlus Account and other savings accounts in this list. Plus, if you maintain an account balance above RM10,000 every month, you will also enjoy waivers for the following transactions: MEPS withdrawals, interbank funds transfers, interbank GIRO, and even the debit card annual fee.

Interest rate: tiered, up to 3.75 per cent p.a.

Interest rate: tiered, up to 3.75 per cent p.a.

The most recent member of the “high interest savings account in Malaysia” club, UOB Stash offers bonus interest when you maintain or increase your account balance every month. Interestingly, UOBStash gives out the highest interest when your account balance is maintained at a range of RM50,000 to RM100,000, as zero bonus interest is given on account balances above RM100,000 (though the base interest is bumped to 2.75 per cent p.a.).

Overall, the effective interest rate that you can earn from the UOB Stash account is 3.25 per cent p.a. for balances between RM50,000 to RM100,000, and only 3 per cent p.a. for balances above RM100,000.

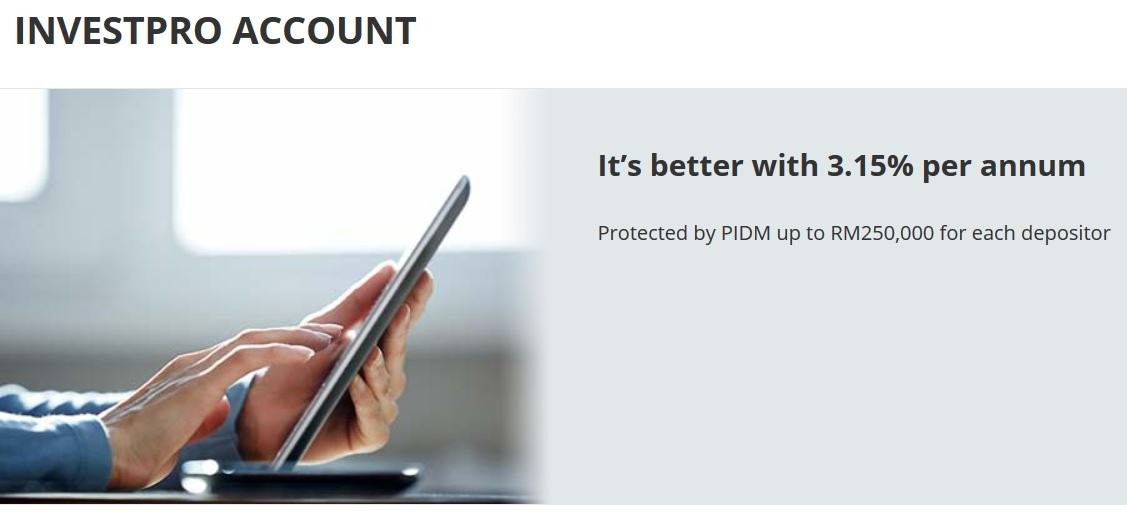

Interest Rate: tiered, up to 3.15 per cent p.a.

Interest Rate: tiered, up to 3.15 per cent p.a.

Formerly known as the UOB eAccount, the UOB InvestPro account is another straightforward savings account that offers huge interest rates without requiring you to perform other transactions with the bank. Its highest 3.15 per cent p.a. interest tier is only unlocked when your total account balance is above RM50,000.

It is marginally lower than UOB Stash’s interest rate for deposits of RM50,000 and above, but the InvestPro wins out in effective interest rate when for balances above RM100,000 (3.15 per cent vs 3 per cent). But if you’ve got RM100,000 to park, Alliance SavePlus trumps both UOB accounts.

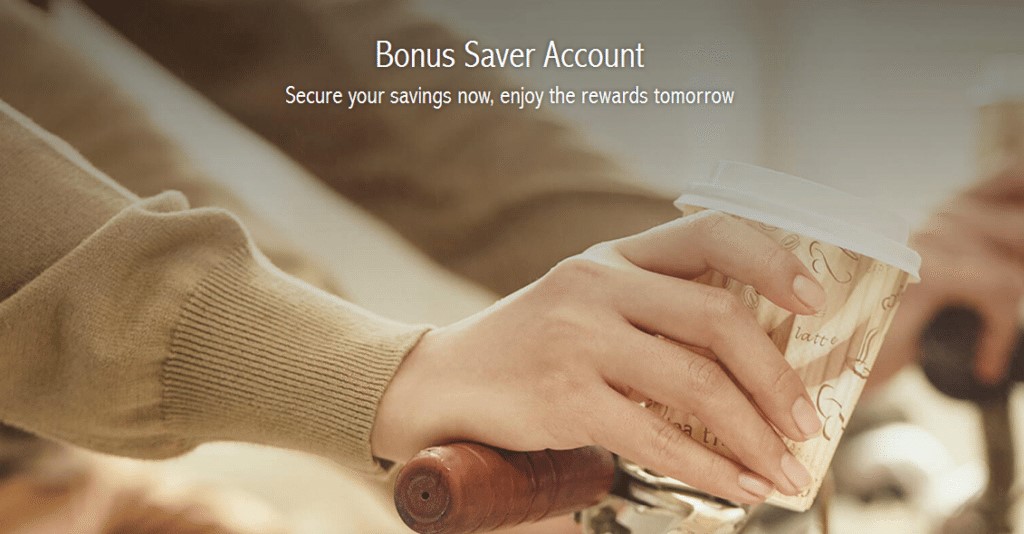

Interest: tiered, up to 2.75 per cent p.a.

Interest: tiered, up to 2.75 per cent p.a.

This savings account is great at rewarding those who save regularly every month. That’s because the RHB Bonus Saver requires you to maintain a monthly incremental balance of RM500 every month for 12 months consecutively to unlock (and retain!) a base interest rate of 2.65 per cent p.a. thereafter. If you continue to have a monthly incremental balance of RM500 every month after the first 12 months, you’ll earn an additional 0.10 per cent p.a. interest for an impressive 2.75 per cent p.a. total.

The RHB Bonus Saver account is great for those who are building up their funds, unlike the UOB’s InvestPro and Stash accounts or the Alliance SavePlus, both of which reward those who deposit large sums of money.

MBSB Cash Rich Savings Account-i

Profit rate: 2.68 per cent p.a.

A lesser-known alternative is the MBSB Cash Rich Savings Account-i, which offers a fantastic rate of 2.68 per cent p.a. for ALL balances. There are no other conditions, which makes it a really good choice for those without huge funds to meet the minimum balance requirements for accounts like the Alliance SavePlus or the two UOB accounts.

As a full-fledged Islamic bank, all MBSB accounts are Syariah-compliant.

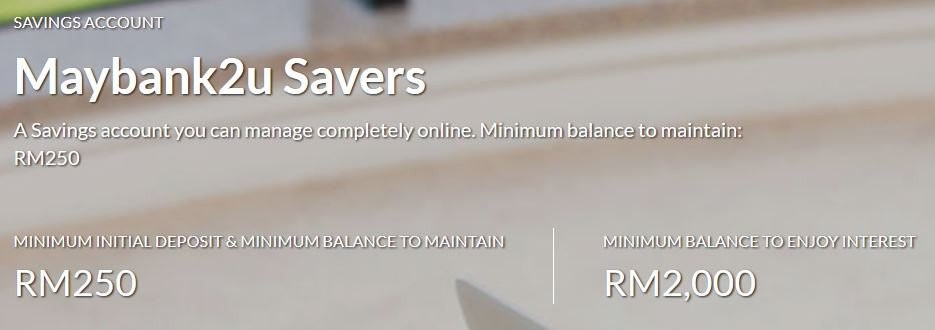

Interest rate: tiered, up to 2 per cent p.a.

Interest rate: tiered, up to 2 per cent p.a.

What used to be the best savings account for the everyday Malaysian has become a shadow of its former self. The M2u Savers and its Syariah-compliant variant, M2u Savers-i, both used to offer as much as 2.5 per cent p.a. interest with a minimum balance of RM2,000. After the recent OPR revision by Bank Negara Malaysia, the M2u Savers account now offers 1.85 per cent for account balances from RM2,000 to RM50,000, and 2 per cent p.a. for all balances above RM50,000.

Final notes

All savings account listed here are insured by PIDM for up to RM250,000, which means that in the event the bank goes bankrupt, your savings account with that bank is insured and can be claimed up to RM250,000.

In addition, there are a few other savings accounts with competitive interest rates that are not listed here. We omitted these as the requirements to unlock those rates are complicated — the ones mentioned here are straight forward, and the requirements are clearly spelt out. But if you do find a savings account with better rates than those listed here, let us know!

*This article was brought to you by RinggitPlus.com.