")

MAY 9 — The global consensus reached at COP28 on the urgent need to transition away from fossil fuels towards cleaner energy systems has sparked growing interest among governments and businesses in both emerging and advanced sources of clean energy to achieve the Paris Agreement targets.

The call to accelerate the deployment of clean energy, including nuclear power, as part of the COP28 negotiated outcome and First Global Stocktake reflects increasing recognition that nuclear energy has a key role to play in clean energy transitions.

This marks the first time nuclear energy has been formally specified as one of the solutions to climate change in a COP agreement. World Nuclear Association Director General Sama Bilbao y León noted that “this marks a 180° turn-around in the treatment of nuclear energy in the COP process, from the lone technology excluded from the Kyoto Protocol mechanisms to COP28’s inclusion among a range of zero and low-emissions technologies.”

Emerging and advanced technologies, including small modular reactors (SMRs), are increasingly promoted as key solutions to decarbonise energy systems, achieve net-zero targets, and meet rapidly growing electricity demand. They are attracting growing interest from governments, utilities and technology companies.

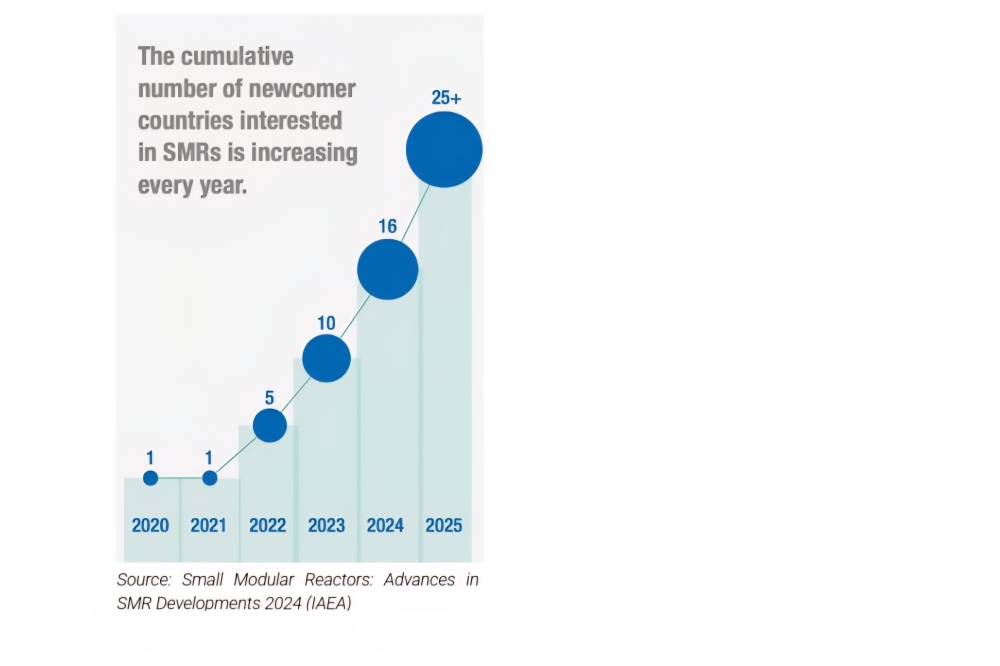

The International Atomic Energy Agency has reported that, as of 2024, governments from 25 countries are exploring SMRs.

Fig 1: The cumulative number of newcomer countries interested in SMRs is increasing every year

Nuclear energy is central to Southeast Asia’s energy conversation.

At the Singapore International Energy Week 2025 (SIEW2025), World Nuclear Association Director General Dr Sama Bilbao y León said nuclear energy is now at the centre of Southeast Asia’s energy discussions, with many ASEAN countries viewing it as an essential component for providing 24/7, affordable and clean electricity.

She added that Asia is projected to account for 30% of the global nuclear share by 2030, with growing interest in small modular reactors (SMRs) to meet rising power demand and decarbonise heavy industry.

Fig 2: Ms Sheriffah had the honour and pleasure of meeting World Nuclear Association (WNA) Director General Sama Bilbao y León at SIEW2025, who also served as moderator at the Roundtable Think Tank on Nuclear Power, of which Sheriffah was one of the panellists.

SMR developers and vendors are making efforts to improve the safety, economic efficiency and modularity of their products.

ABI reported that many SMR vendors are working to enhance these aspects, with companies such as GE Vernova, Hitachi Energy, NuScale, Rolls-Royce, Holtec, Oklo and X-energy investing billions of dollars into constructing SMRs across North America and Europe over the next decade.

Fig 3: Global SMR System Leaders

ABI Research

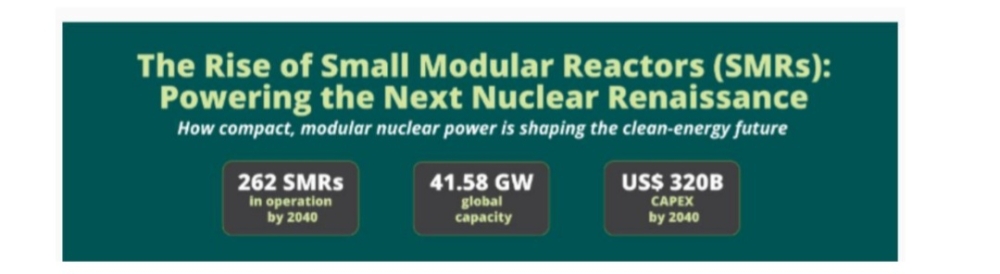

According to ABI Research, the accumulated Capital Expenditure (CAPEX) spent on SMR construction is projected to eclipse US$320 billion between 2025 and 2040. (Fig 4)

Fig 4: The Rise of Small Modular Reactors (SMRs)

Growing consensus

There is a growing consensus that small modular reactors (SMRs) could be a viable option for meeting net-zero emissions targets, with strong interest, enthusiasm and investment from governments, utilities and technology companies. Relying on nuclear energy, including SMRs, is also seen as one strategy for major technology firms to avoid missing their net-zero commitments while scaling up energy-intensive artificial intelligence systems. In March 2024, Utility Dive estimated that the United States had nearly 4 gigawatts (GW) of publicly announced SMR projects, alongside almost 3 GW in early-stage development. However, scepticism remains over SMRs’ ability to deliver on their promises. While interest in SMRs as a clean energy source is growing, questions persist about their commercial viability and scalability.

Projected attributes of SMRs and cause for caution

Proponents of SMRs argue that, compared with conventional large nuclear reactors, they are faster to build, more cost-effective, require lower upfront capital, have a smaller footprint and offer enhanced safety. These attributes have driven significant interest and investment globally. However, with only two SMRs currently operating commercially worldwide — one in Russia and one in China — several analysts argue that many of these claims remain largely unproven. Past SMR projects that were cancelled or abandoned, along with cost overruns and construction delays in existing projects, have further fuelled caution. In addition, many challenges facing conventional nuclear power — including lengthy licensing processes, high upfront costs, constrained fuel supply chains and unresolved waste management issues — remain equally relevant for SMRs.

Aborted and abandoned SMR projects

Energy Intelligence reported on 17 November 2023 that the collapse of the US Department of Energy’s flagship SMR project, Babcock & Wilcox’s “mPower” design, which received early funding in 2012 and collapsed in 2017, should serve as a cautionary example. Similarly, NuScale Power’s Carbon Free Power Project (CFPP) with Utah Associated Municipal Power Systems (UAMPS), launched in 2013 and terminated in November, also highlighted key commercial risks. The project struggled to secure sufficient utility participation, especially after projected electricity prices rose significantly from about $58/MWh to $89/MWh — an increase of 53 per cent.

Current commercially operating SMRs — Russia and China

Russia’s floating nuclear power plant (FNPP)

The World Nuclear Industry Status Report 2021 highlighted Russia’s Akademik Lomonosov floating nuclear power plant as a prototype SMR. Initially expected to begin operation in 2010, it only entered service in December 2019, reflecting a construction delay of nearly a decade. Costs also escalated significantly, rising from about 6 billion rubles (US$2007 ~232 million) to at least 37 billion rubles by 2015 (US$2015 ~740 million), or close to US$25,000 per installed kilowatt — nearly twice the cost of the most expensive Generation III reactors.

China’s high-temperature gas-cooled reactor (HTGR)

China’s demonstration twin-reactor HTGR is another operating SMR. The World Nuclear Association estimates its cost at around US$6,000 per kilowatt, roughly three times higher than initial projections and significantly above the cost of China’s larger Hualong reactors. NucNet reported in 2020 that China later dropped plans to mass-produce 20 HTGR units after levelised cost estimates exceeded those of conventional large reactors.

The path to commercial viability remains uncertain

According to the OECD Nuclear Energy Agency, the economic viability of SMRs depends on the development of a large global market. However, achieving this scale faces technical, economic, regulatory and supply chain challenges, requiring strong government support and international coordination. The International Atomic Energy Agency (IAEA) has noted that around 80 SMR designs are currently under development globally. However, the large number of competing technologies makes it difficult for any single design to achieve economies of scale. Geopolitical Intelligence Services (GIS) has also noted that most SMR designs remain unproven at scale, with their full economic, regulatory and operational implications likely to only become clear after broader deployment.

Reality of past SMRs: spotlighting construction schedule, regulatory process and cost

1. The construction schedule: SMRs do not necessarily take a shorter time to build

Evidence from past and current projects shows that SMRs do not automatically result in shorter construction timelines. While they are promoted as faster to deploy due to their smaller size and modular design, real-world projects have often faced significant delays similar to conventional reactors. The experience suggests that “small” does not necessarily translate into “fast,” especially when regulatory, engineering and supply chain complexities are factored in.

2. Regulatory process of SMRs

SMRs still go through the same rigorous nuclear regulatory frameworks as larger reactors, including safety assessments, design certification and site approvals. In many cases, new SMR designs require additional regulatory scrutiny because they introduce novel technologies and configurations. This can extend approval timelines and reduce the expected speed advantage often associated with modular deployment.

3. The cost comparison: SMRs are not necessarily cheaper than conventional reactors

Smaller modular reactors are generally cheaper to build in absolute terms than large reactors, but they tend to be more expensive per megawatt (MW) of electricity generated due to economies of scale. While reducing plant capacity lowers total construction cost, the reduction is not proportional, making cost per unit of power higher.

The “modular” concept — involving mass production of standardised components assembled on-site — is essential to improving economic viability. However, significant on-site construction is still required. Moreover, many large conventional reactors already incorporate modular construction techniques, raising questions over whether SMRs can meaningfully reduce costs beyond existing technologies.

True cost advantages depend heavily on large-scale mass production, meaning only a limited number of designs are likely to achieve global commercial deployment.

The collapse of NuScale’s SMR project in the United States highlights these challenges. In 2020, the U.S. Department of Energy approved a cost-share award of up to US$1.4 billion for a 12-module NuScale plant at Idaho National Laboratory under Utah Associated Municipal Power Systems (UAMPS). The U.S. Nuclear Regulatory Commission certified NuScale’s design in January 2023, making it the first SMR design certified in the country.

However, by October 2023, projected electricity costs had risen by 53 per cent compared to initial estimates, already exceeding the cost of utility-scale solar and wind power. Despite government funding support, UAMPS terminated the project in November 2023 due to insufficient subscription commitments as costs continued to escalate. By that stage, the project had received around US$232 million in U.S. Department of Energy funding.

Recommendations to the Government of Malaysia

Given the track record of cancelled SMR projects, as well as cost escalations and delays in existing deployments, it is essential that the Government of Malaysia — along with public and private energy stakeholders — carefully evaluate both the advantages and limitations of SMRs before making investment decisions. A comprehensive review comparing SMRs with conventional large nuclear reactors, based on proven safety records, financial performance and other key parameters, should be undertaken. This would help ensure that Malaysia selects the most suitable, safe and economically viable nuclear energy pathway for the country and its people.

*Sheriffah Noor Khamseah Al-Idid bt Dato Syed Ahmad Idid (Consultant Nuclear Power, Venture Capital and Innovation)

** This is the personal opinion of the writer or publication and does not necessarily represent the views of Malay Mail